What Is the Nominal Interest Rate? Why the Price of Money Matters for Stocks, Real Estate, and Currency Markets

Hello, this is MasterMind.

Why does the stock market react so strongly every time the Federal Reserve raises or cuts interest rates?

Why did home prices surge during the low-rate era after the pandemic, only to cool down as borrowing costs moved higher?

And why do investors pay as much attention to interest rate decisions as they do to corporate earnings reports?

The answer begins with one of the most important concepts in finance - the nominal interest rate.

Most people think of interest rates as the number attached to a savings account, mortgage, or credit card. In reality, nominal interest rates are far more important than that.

They influence how much it costs to borrow money, how attractive investments appear, how capital moves around the world, and ultimately how assets are priced.

Whether you invest in stocks, bonds, real estate, gold, or Bitcoin, understanding nominal interest rates is one of the foundations of understanding financial markets.

Key Takeaway

The nominal interest rate is the stated interest rate before adjusting for inflation. It serves as the price of money throughout the economy and plays a central role in determining liquidity, asset valuations, and capital flows.

What Is the Nominal Interest Rate?

The nominal interest rate is the interest rate that appears on financial products and contracts without accounting for inflation.

Examples include

- Savings account rates

- Mortgage rates

- Corporate borrowing costs

- Treasury yields

- The Federal Funds Rate

When a bank offers a 5% savings account, that 5% is the nominal interest rate.

However, if inflation is running at 3%, your purchasing power is not increasing by the full 5%.

This is why economists distinguish between nominal interest rates and real interest rates.

While the real interest rate reflects purchasing power after inflation, the nominal interest rate represents the visible cost of borrowing and the visible return on lending.

For investors, both matter.

But when it comes to liquidity and capital flows, nominal interest rates are often the first variable that drives market behavior.

How Are Nominal Interest Rates Determined?

Nominal interest rates do not move randomly.

They are influenced by several powerful economic forces.

Federal Reserve Policy

The Federal Reserve has the greatest influence on short-term interest rates in the United States.

When the Fed raises rates, borrowing becomes more expensive.

When the Fed lowers rates, borrowing becomes cheaper.

This gives policymakers a powerful tool to cool down inflation or stimulate economic activity.

Inflation Expectations

Investors care about future purchasing power.

If inflation is expected to rise, lenders typically demand higher interest rates to compensate for the anticipated loss in value of future dollars.

As a result, higher inflation expectations often push nominal interest rates upward.

Economic Growth

Strong economic growth generally increases demand for capital.

Businesses borrow more money to expand operations, invest in equipment, and hire workers.

As demand for capital rises, interest rates often move higher.

During economic slowdowns, the opposite tends to occur.

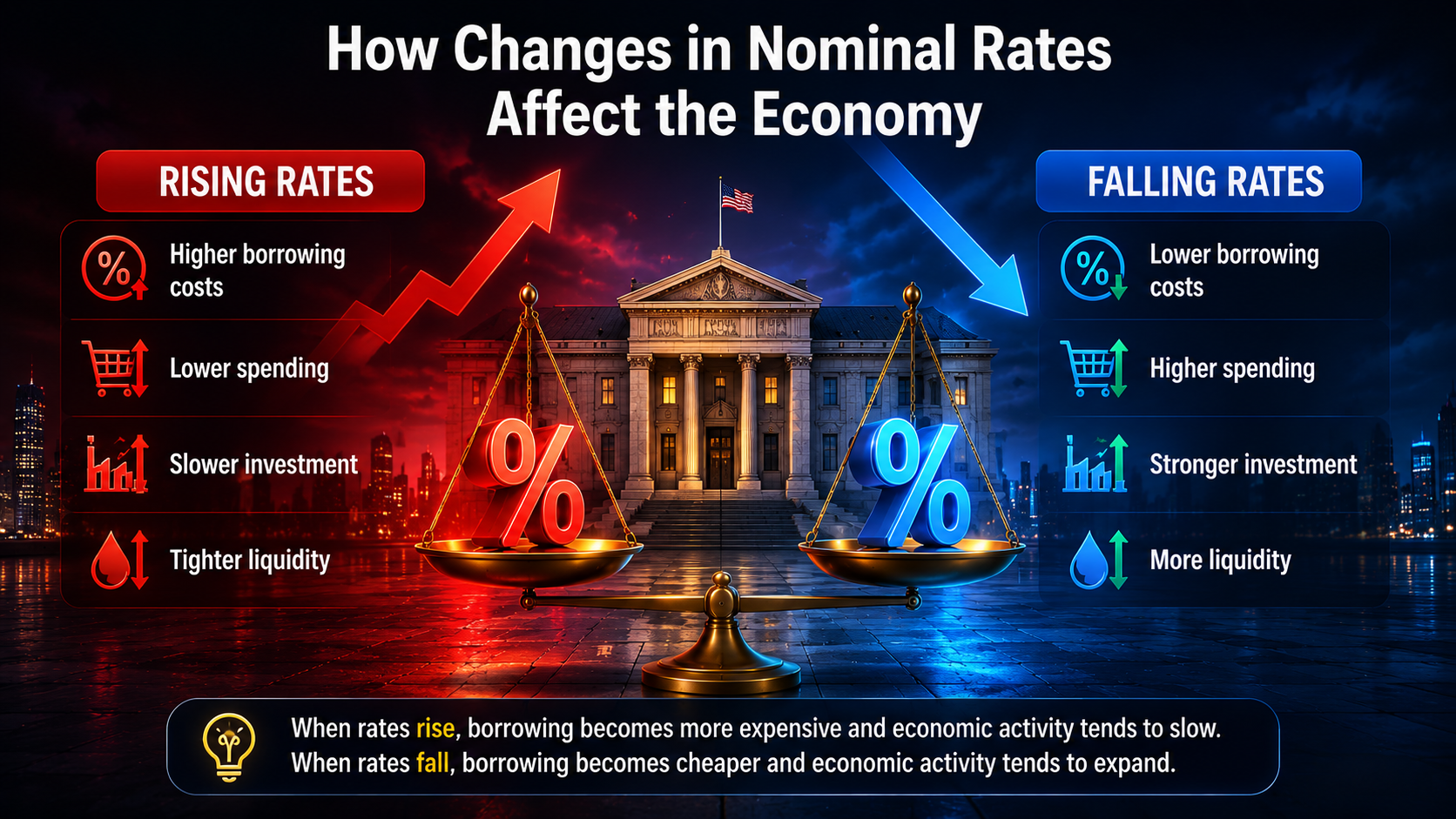

How Nominal Interest Rates Influence Liquidity

One of the best ways to think about nominal interest rates is to view them as the control valve of financial liquidity.

When Interest Rates Rise

Higher rates increase the cost of borrowing.

As a result

- Consumers reduce spending

- Businesses delay expansion plans

- Mortgage demand declines

- Financial conditions tighten

Money flows more slowly through the economy, reducing overall liquidity.

When Interest Rates Fall

Lower rates reduce borrowing costs.

As a result

- Consumer spending increases

- Business investment expands

- Housing demand improves

- Investors seek higher returns in risk assets

Liquidity becomes more abundant, often supporting economic growth and asset prices.

This is why interest rate cycles are closely tied to market cycles.

Why Investors Pay Attention to Nominal Interest Rates

Many investors focus primarily on earnings, economic data, or market sentiment.

However, interest rates influence something even more fundamental

the price of money itself.

Every investment decision begins with comparing risk and reward.

If investors can earn attractive returns from low-risk Treasury securities, they become more selective about taking risk elsewhere.

As nominal interest rates rise, stocks, real estate, and other risk assets must compete against increasingly attractive alternatives.

This process directly affects asset valuations.

In many ways, interest rates act as the foundation upon which all financial markets are built.

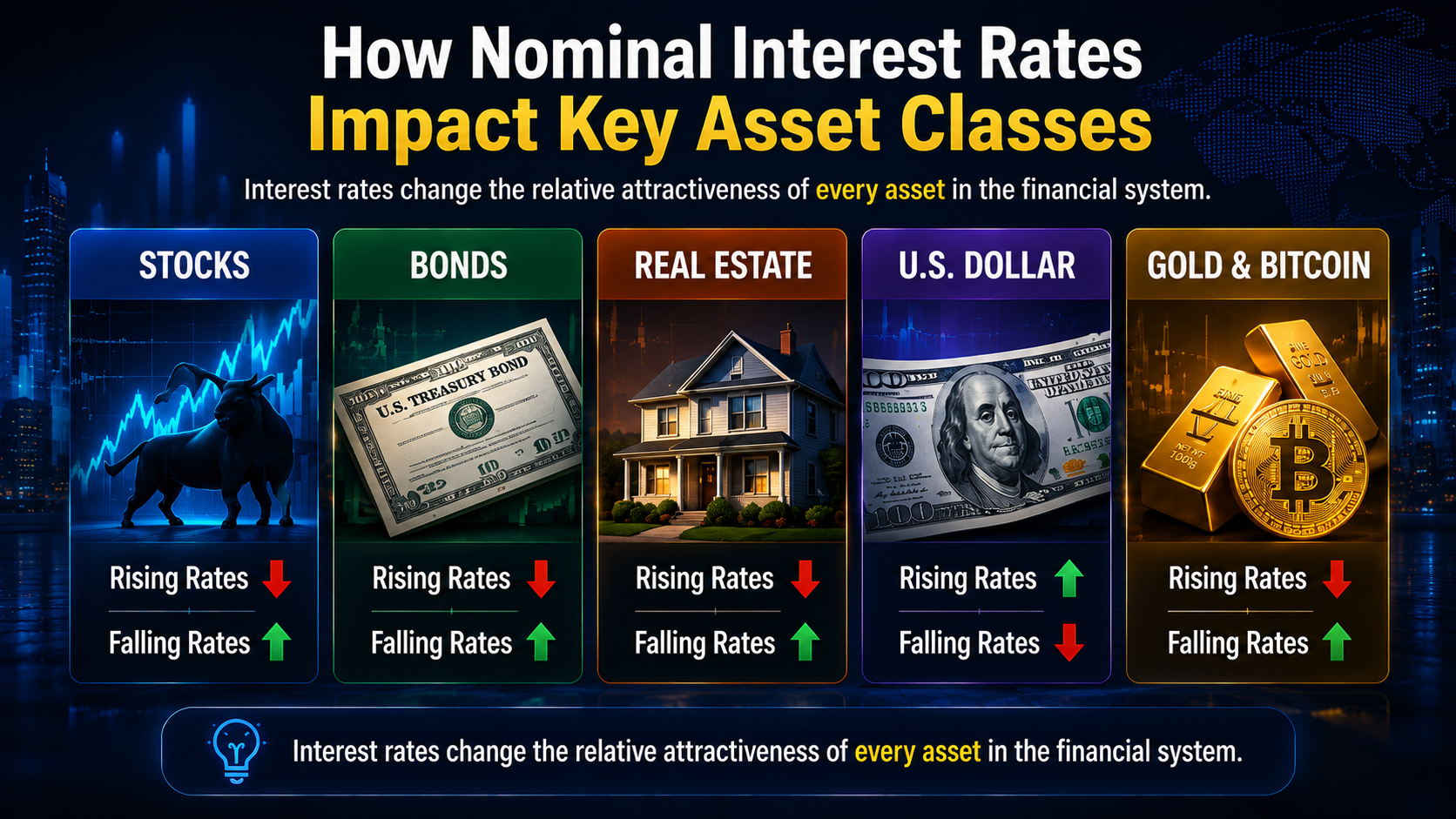

How Nominal Interest Rates Affect Major Asset Classes

| Asset Class | Impact of Rising Rates | Impact of Falling Rates |

| Stocks | Valuation pressure | Valuation expansion |

| Bonds | Prices typically fall | Prices typically rise |

| Real Estate | Lower affordability and demand | Increased affordability and demand |

| U.S. Dollar | Often strengthens | Often weakens |

| Gold | Faces higher opportunity cost | Often benefits |

| Bitcoin | Liquidity tends to tighten | Liquidity tends to expand |

Stocks

Stocks represent future cash flows.

As interest rates rise, those future earnings are discounted more heavily, reducing present valuations.

Growth stocks are often the most sensitive because a larger portion of their value depends on profits expected years into the future.

Real Estate

Real estate is highly dependent on financing.

When mortgage rates rise, affordability declines.

This often reduces housing demand and slows transaction activity.

Lower rates generally have the opposite effect.

Currency Markets

Capital tends to flow toward higher yields.

When U.S. interest rates rise relative to those of other countries, international investors may move capital into dollar-denominated assets.

This often strengthens the U.S. dollar.

Key Lessons for Investors

Focus on Direction, Not Just Level

Markets are forward-looking.

Often, what matters most is not where rates are today, but where investors believe rates will be six to twelve months from now.

This is why markets sometimes rally before the Fed actually begins cutting rates.

Watch Long-Term Treasury Yields

The Federal Reserve controls short-term policy rates.

The bond market influences long-term rates.

Investors should monitor both because long-term Treasury yields often reflect future economic expectations.

Liquidity Matters as Much as Rates

Low rates alone do not guarantee rising asset prices.

Investors should also pay attention to

- Money supply growth

- Quantitative easing (QE)

- Quantitative tightening (QT)

- Credit conditions

- Treasury market liquidity

Interest rates and liquidity work together to shape financial markets.

What Do Wealthy Investors Look For?

Experienced investors rarely view interest rates as simply bullish or bearish.

Instead, they focus on how money moves throughout the financial system.

Markets are ultimately driven by capital flows.

When rates rise, money often shifts toward safer assets.

When rates fall, capital frequently seeks higher returns in riskier investments.

Wealthy investors also pay close attention to cash flow durability.

Rather than asking whether an asset will rise next month, they ask

- Can this asset survive higher interest rates?

- Does it generate reliable cash flow?

- Can it withstand an economic slowdown?

- Will it remain valuable ten years from now?

The goal is not to predict every market move.

The goal is to own assets that can survive across multiple economic environments.

In investing, survival often matters more than forecasting.

Final Thoughts

Nominal interest rates are far more than the numbers displayed on a savings account or mortgage statement.

They influence borrowing costs, liquidity conditions, investment decisions, and the valuation of nearly every major asset class.

Understanding nominal interest rates means understanding how money moves through the economy.

And investors who understand the flow of money are often better positioned to recognize opportunities and risks before they become obvious to everyone else.

The most important lesson is simple

Nominal interest rates are the price of money, and the price of money influences the direction of nearly every financial market.

This was MasterMind.

'[Global] Success Blueprints' 카테고리의 다른 글