U.S. Stock Capital Gains Tax Guide for Korean Investors -Deductions, Tax-Loss Harvesting, and Family Gifting Strategies

Hello, this is MasterMind.

Many investors enter the U.S. stock market attracted by the growth potential of companies like Nvidia, Microsoft, Apple, and Amazon. They spend countless hours searching for the next winning stock, yet often overlook one of the most important aspects of investing: taxes.

In reality, your true investment return is not what appears on your brokerage statement. It is what remains after taxes.

The difference between successful investors and wealthy investors is often not the ability to generate returns, but the ability to preserve them.

Today, we will explore how Korean investors can legally reduce taxes on U.S. stock investments through capital gains tax planning, the annual ₩2.5 million deduction, tax-loss harvesting, and family gifting strategies.

Understanding U.S. Stock Capital Gains Tax for Korean Investors

One common misconception is that profits from U.S. stocks are taxed by the United States.

For Korean residents, capital gains from U.S. stocks are generally reported and taxed under Korean tax law.

The key principle is straightforward:

All gains and losses from overseas stock investments during a calendar year are combined to determine your net taxable profit.

This means profitable investments and losing investments are not treated separately. Instead, they are aggregated before taxes are calculated.

Understanding this mechanism is the foundation of every effective tax-saving strategy.

How Capital Gains Tax Is Calculated

The process is relatively simple.

- Calculate total annual gains and losses from overseas stocks.

- Determine your net profit.

- Apply the annual deduction of ₩2.5 million.

- Pay a 22% tax on the remaining taxable amount.

Let's look at a practical example.

- Nvidia gain: ₩10,000,000

- Tesla loss: ₩3,000,000

First, calculate your net profit.

Net Profit = ₩10,000,000 − ₩3,000,000 = ₩7,000,000

Next, apply the annual deduction available to Korean investors.

Taxable Income = ₩7,000,000 − ₩2,500,000 = ₩4,500,000

Finally, apply the combined capital gains tax rate of 22%, which includes local income tax.

Estimated Tax = ₩4,500,000 × 22% = ₩990,000

In this example, the investor generated ₩7 million in net profit, reduced the taxable amount through the annual deduction, and ultimately owed approximately ₩990,000 in taxes.

This example highlights why tax-loss harvesting and the annual deduction are powerful tools for improving after-tax investment returns. Managing losses strategically can be just as important as generating gains.

Key Changes Investors Should Pay Attention To

1. The Number of U.S. Stock Investors Continues to Grow

Over the last decade, Korean investors have dramatically increased their exposure to U.S. equities.

As participation grows, tax compliance and tax planning become increasingly important.

Investors who ignore taxes may discover that a significant portion of their gains disappears when tax season arrives.

2. The Annual ₩2.5 Million Deduction Is Use-It-Or-Lose-It

One of the most valuable benefits available to Korean investors is the annual capital gains deduction of ₩2.5 million.

However, many investors fail to maximize it.

The deduction does not carry forward to future years.

If you do not use it this year, it disappears permanently.

This is why sophisticated investors often realize gains strategically before year-end, especially when accumulated gains remain below the deduction threshold.

By doing so, they can gradually reset their tax position while minimizing future tax liabilities.

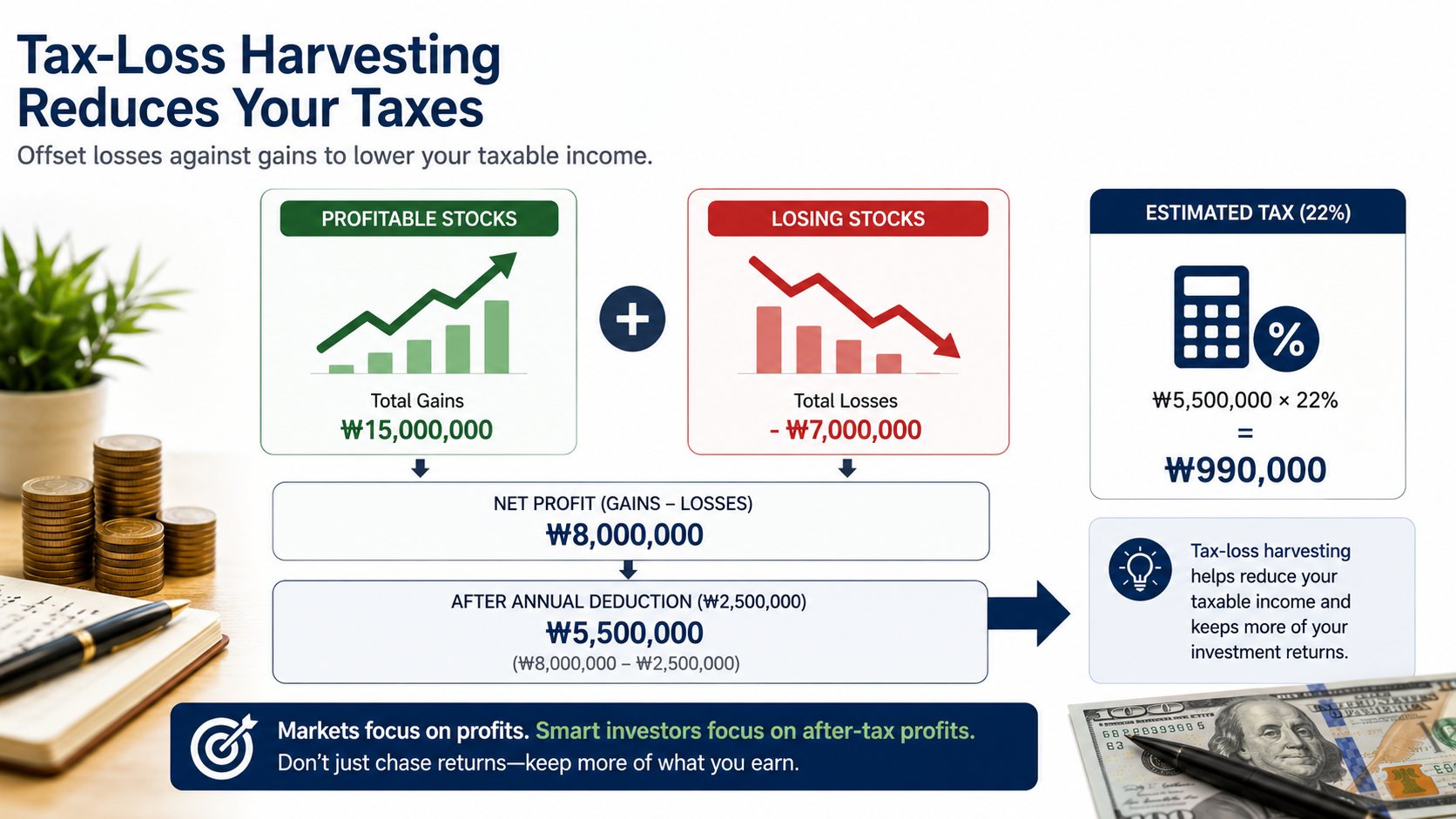

3. Tax-Loss Harvesting Can Significantly Reduce Taxes

Many investors view losing positions as failures.

Professional investors often view them as tax assets.

Consider the following example:

- Capital gains: ₩15 million

- Capital losses: ₩7 million

Net taxable gain becomes:

₩8 million

After applying the annual deduction, taxable income falls even further.

This strategy, commonly known as tax-loss harvesting, allows investors to offset gains and lower their overall tax burden.

The market focuses on profits.

Wealthy investors focus on after-tax profits.

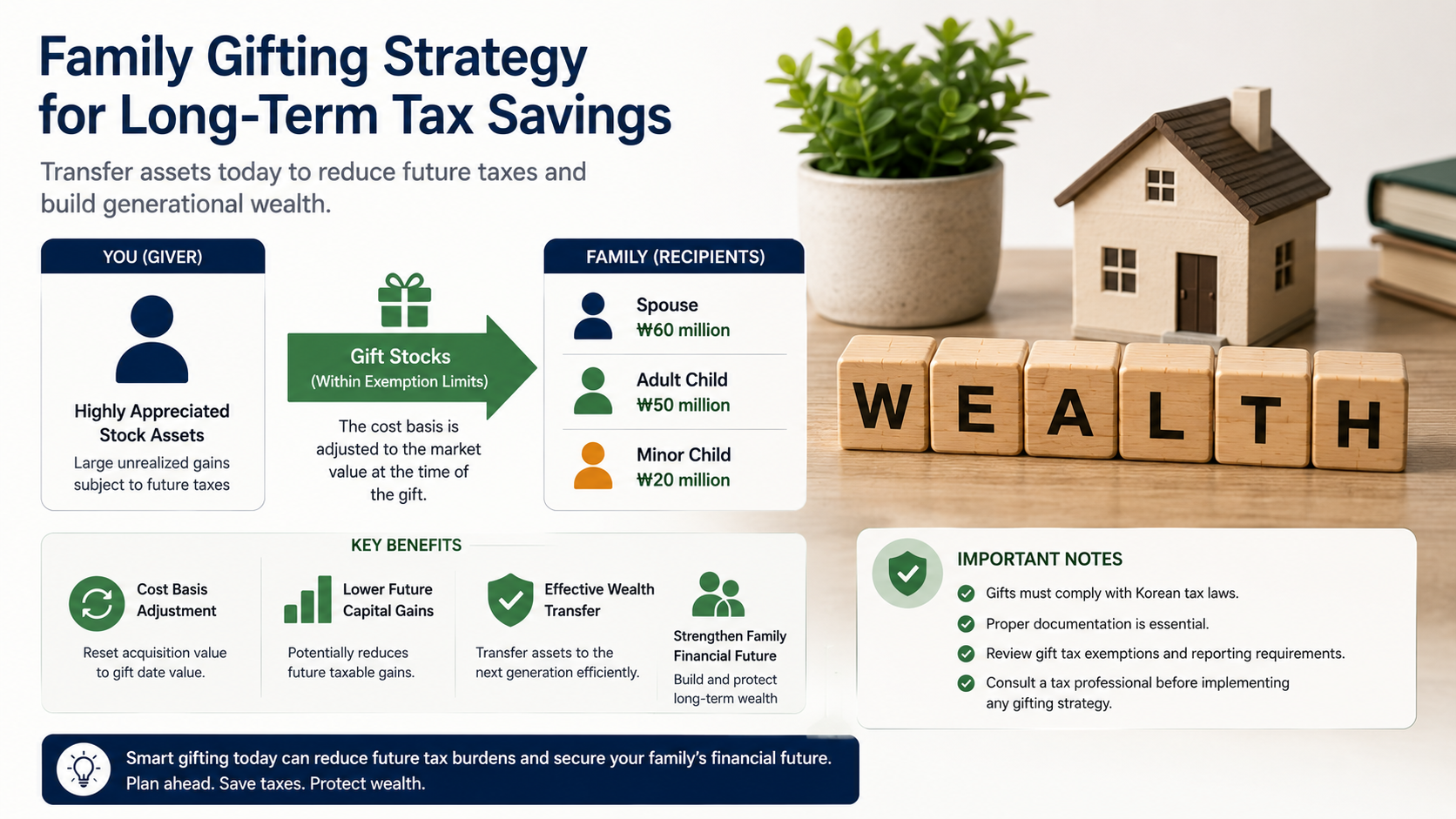

4. Family Gifting Can Be a Powerful Wealth Transfer Strategy

One of the most advanced tax-planning strategies involves transferring appreciated assets to family members.

Under Korean tax rules, gift tax exemptions may apply within certain limits for spouses and children.

The major advantage is the adjustment of the cost basis.

When shares are gifted, the recipient's acquisition value is generally recalculated based on the valuation at the time of the gift.

As a result, future capital gains may be significantly reduced.

For long-term investors holding stocks with substantial unrealized gains, this strategy can become an important part of intergenerational wealth planning.

However, proper documentation, compliance, and professional advice are essential before implementing any gifting strategy.

Risks Investors Should Not Ignore

Tax planning is valuable, but mistakes can be costly.

Several risks deserve attention.

Settlement Date Confusion

Tax reporting generally depends on settlement dates rather than trade dates.

Waiting until the final days of the year to execute a tax strategy can create unexpected reporting issues.

Currency Risk

U.S. stocks are traded in dollars, but taxes are calculated in Korean won.

Exchange-rate fluctuations can affect taxable gains even when stock performance remains unchanged.

Health Insurance and Dependent Status

Using family members' accounts or gifting strategies may influence eligibility for dependent deductions or health insurance benefits.

Tax savings should always be evaluated alongside potential secondary consequences.

Improper Gifting Structures

If a gift lacks economic substance or fails to meet legal requirements, tax authorities may challenge the transaction.

A successful strategy requires both tax efficiency and regulatory compliance.

What Do Wealthy Investors See in This Trend?

Wealthy investors rarely focus solely on returns.

They focus on preserving capital and controlling cash flows.

Every dollar saved in taxes remains available for reinvestment.

Over time, this creates a powerful compounding effect.

While most investors ask:

"How much can I make?"

Wealthy investors ask:

"How much can I keep?"

This difference in mindset often explains the difference in long-term wealth outcomes.

Ask yourself:

- Do I know my expected after-tax return?

- Am I fully utilizing annual tax deductions?

- Am I harvesting losses when appropriate?

- Do I have a long-term family wealth transfer plan?

These questions matter more than predicting next month's market move.

Final Thoughts

Investing is not simply about finding great companies.

It is also about understanding the rules of the game.

For Korean investors in U.S. stocks, the annual ₩2.5 million deduction, tax-loss harvesting opportunities, and family gifting strategies can play a significant role in preserving wealth.

Markets reward those who generate returns.

But over the long run, they reward even more those who protect them.

MasterMind's Take

The market determines how much opportunity is available.

Your tax strategy determines how much of that opportunity ultimately becomes wealth.

In investing, survival matters more than prediction, and preserving capital is often the foundation of long-term success.

This was MasterMind.

'[Global] Success Blueprints' 카테고리의 다른 글